People don’t talk about it quite as much as they did in 2008, but big banks are the worst. Aside from the fact that

they’re full of crooks, big banks provide terrible customer service, charge obscene fees, and profit from your misery. You should probably stop giving them your money now.

Unfortunately, short of keeping sweaty wads of cash in shoeboxes under your waterbed, quitting big banks is a difficult thing to do. A lot of startup financial services companies

are actually backed by corporate giants, as quietly funding a startup is a good way for those vampires to suck your blood without your realizing it. Heck, even small banks that don’t rip you off eventually get acquired by big banks.

There is hope, however. You can cut yourself out from big banks. It’s entirely possible to never set foot in a bank again and lead an enriched, financially responsible lifestyle.

I’m not just talking about going all-mobile, either. Plenty of people just use their big bank’s app to deposit checks and their (practically prehistoric) debit card to get cash out at an ATM without ever visiting the brick-and-mortar institution. You can take it a stage further and just close all those big bank accounts. That’s what I did.

I’ve spent the past five years experimenting in the many methods of banking, both with startups and with the big banking giants. These are the best apps and services I’ve found. And I use each of them on an almost daily basis.

My decision to quit big banks

I’ll admit it: I made some financially irresponsible decisions in my twenties. In college, I was almost always one overdraft fee away from going hungry. When I moved to the city for my first job, I’d blow through my paycheck in the blink of an eye.

So when Bank of America—the bank that tricked me into opening an account in college with a free lunchbox or something—would go on one of its fee sprees, my quality of life decreased. You know the kind of thing I’m talking about: one overdraft fee triggers another, and the next thing you know, you’re $300 in the red. Not only would I be broke, I’d also have to fudge my way through a robotic phone call for half an hour before I could talk to a real human and straighten out the fees—which were often charged to me in error.

A couple years later, Chase tricked me into opening an account with a free $100. It only took them a few months to win back that amount in the form of hidden fees. (Protip: if you don’t keep a huge balance or do direct deposit with your Chase checking account, you’ll get charged a slick $12 a month.) That’s when I finally came to the realization that all of these big, shitty banks truly are big and shitty—and don’t even get me started on the big banks’ generous contributions to the horror that was the financial crisis. I was sick of it all.

That’s when Simple came along.

A non-shitty checking account: Simple

You’ve

probably heard about Simple by now. The four-year-old startup was founded as a mobile-focused alternative to big banks. Although Simple moved out of the startup category earlier this year, when it was acquired by the decidedly not-startup bank BBVA, the sales pitch remains, well, simple: “No overdraft, no minimums, no worries.”

I started using Simple as my primary checking account about two years ago, and if you’re trying to avoid the bullshit of the big shitty banks, you should do the same right now. Simple is indeed an all-mobile banking solution, though you can do just about everything on the web. I should also point out that the service has only improved since the BBVA acquisition, a bank that enjoys unusually good consumer satisfaction ratings despite being big.

Simple also the best banking app I’ve ever used, and I’ve used several at this point. Everything from the quick, passcode-based login to the handle map to free ATMs makes the app a breeze to use. And the fact that there’s not much else besides checking your balance and sending people money is delightful frills-free. You can also suspend your debit card from the app which is wonderfully handy if you misplace your card. You just turn the same card back on from the app. Simple!

What really sets Simple apart, however, is the customer service. You can communicate with the bank’s very human and very friendly support staff in a variety of ways. You can text or email back and forth with them. You can also call and talk to someone immediately without having to fumble through those terrible robo-operators with crappy voice recognition software.

What really sets Simple apart, however, is the customer service. You can communicate with the bank’s very human and very friendly support staff in a variety of ways. You can text or email back and forth with them. You can also call and talk to someone immediately without having to fumble through those terrible robo-operators with crappy voice recognition software.

Anytime I had saw strange activity on my account, Simple would also credit my account, no questions asked, while they looked into the issue. The bank has never once charged me a fee. In fact, I’ve never given them a penny—aside from all the pennies they safely stored in my checking account.

Simple is still adding useful new features, too. The service has always boasted about its Mint-like features that track your spending by category and enable you to set financial goals for yourself. If you still use paper checks, Simple will actually write them for you. Just fill out a little form on the app, and the bank mails the check to its destination. Sending money to friends instantly isn’t quite as easy as it could be. Luckily, however, there’s another terrific, non-evil app for that.

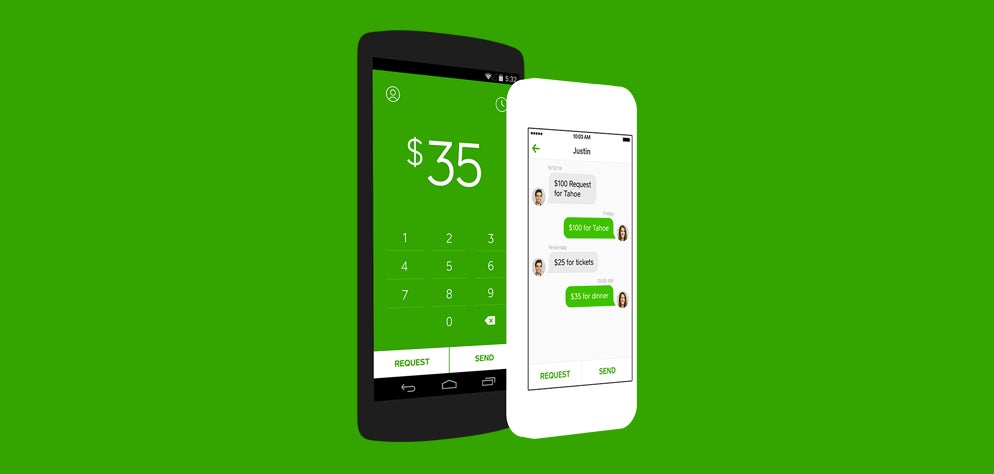

A non-shitty payments app: Square Cash

The battle to dominate the burgeoning digital payments industry is raging more fiercely than ever. PayPal

is literally throwing off dead weight so that it can continue to dominate the space as snoozy services like Google Wallet soldier on. Now even Apple’s trying to elbow its way into the market. As an iPhone 5 user in a cash-loving city, however, I don’t really need all the features that these services offer. More often than not, I just need to pay my friends for my share of dinner or whatever.

Square Cash is the best way to do this. While it’s easy to, say, send funds from one Chase bank account to another, it’s hard to find a dinner table full of friends who all do business at the same bank. Meanwhile, Venmo is one of the original peer-to-peer payments services. But its once-totally free service now carries its own stash of hidden fees. (That activity feed is also kind of creepy.)

So I use Square Cash. The Square spinoff is hilariously easy to use. You just connect a debit card to your account, type in a friends’ email or phone number, and then send them as much money as you want. (Okay not, like, an infinite amount of money. Square caps the weekly transfer amount to $250. If you blow past that, you have to verify your identity, and then you can send $2,500.) The recipient of the payment doesn’t even need to have the app to receive the money. Transfers typically happen instantly, and I’ve never seen one take longer than 24 hours.

So I use Square Cash. The Square spinoff is hilariously easy to use. You just connect a debit card to your account, type in a friends’ email or phone number, and then send them as much money as you want. (Okay not, like, an infinite amount of money. Square caps the weekly transfer amount to $250. If you blow past that, you have to verify your identity, and then you can send $2,500.) The recipient of the payment doesn’t even need to have the app to receive the money. Transfers typically happen instantly, and I’ve never seen one take longer than 24 hours.

Oh, and it’s totally free.

A non-shitty savings account: Venmo

This is going to sound a little bit weird, but bear with me: Try using Venmo as a savings account. Let me rephrase that: If your need for a savings account is similar to mine—that is, if you use it as a method to hide money from yourself so you don’t spend it—you should use Venmo as a savings account.

I don’t use Venmo very often. Like I said a second ago, I find the activity feed to be pretty creepy, and it’s not as easy to cash out as I’d like it to be. But this can be useful if you’re trying to keep your money at arms’ length.

When you first cash out, you’ll have to wait a few days while Venmo makes small deposits in your bank account, and then you’ll have to wait some more for the money to actually transfer. This might not be the case for everyone, every time. However, I recently did a test run, and both steps took several days. That’s time enough for me to reconsider whether or not I really need another pair of selvedge jeans.

When you first cash out, you’ll have to wait a few days while Venmo makes small deposits in your bank account, and then you’ll have to wait some more for the money to actually transfer. This might not be the case for everyone, every time. However, I recently did a test run, and both steps took several days. That’s time enough for me to reconsider whether or not I really need another pair of selvedge jeans.

I’ve been using Venmo for about five years now. Again, I almost never send money with it, but people have sent me money. Since that money was never immediately available and I seldom looked at the app, I pretty much forgot it was there. That’s what gave me the idea to start transferring a slice of every paycheck to Venmo to help my nest egg grow. While I do interact with the app a little more than I used to, I still forget about that money, largely because the balance isn’t staring me in the face every time I log into my checking account.

This is obviously not a perfect solution for a savings account. There’s no interest, but frankly, the interest you get with a standard checking account at any big shitty bank might as well be nothing. And if you keep a large enough balance in your savings account that interest is a real issue, you should be investing that money away in stocks or bonds or other financial products.

Not sure how all that works? Lifehacker has a handy guide.

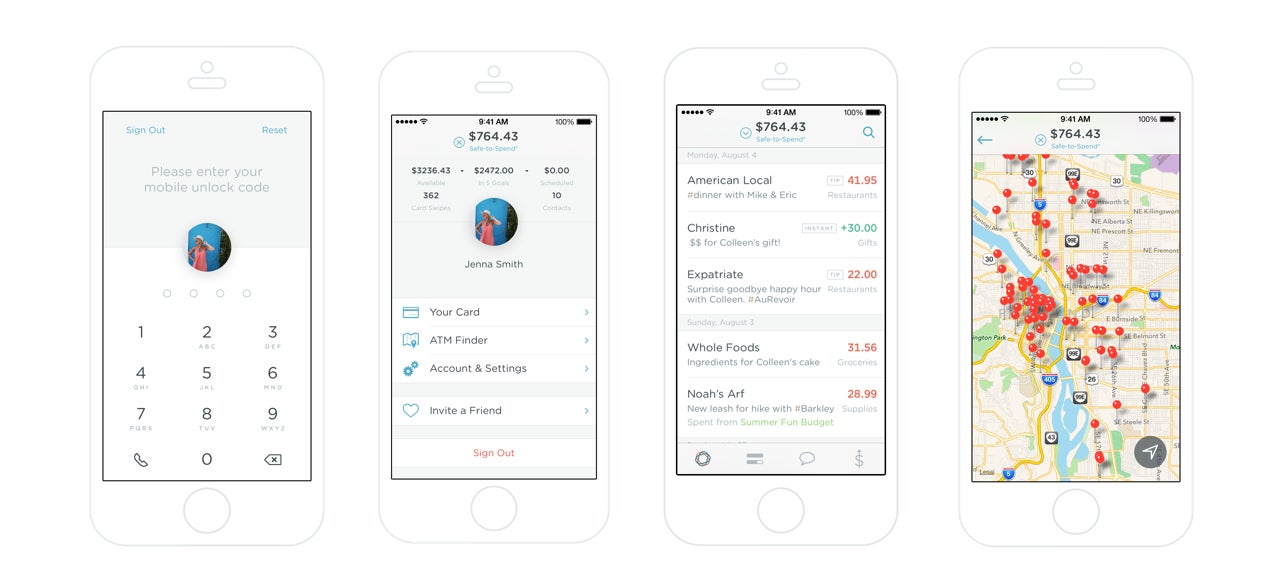

A non-shitty financial planner: Level

Even if you sign up for and start using all of the (highly recommended) services above, it’s still pretty damn easy to make bad financial decisions. The best way to avoid this is to plan better.

This is hardly a revelation. However, while building budgets and tracking spending used to demand you create complex spreadsheets and balance your checkbook regularly, the wonders of computer technology mean that much of the heavy lifting can be done by apps and online services. There are plenty of them out there. While

lots of people use and love Mint, my favorite is a pretty little app called Level.

Level models itself on the classic experience of figuring out how much fun you can have on a Saturday night 1970s-style. Just open your wallet and see how much money is inside. When you’re out of money, you’re done having fun!

The Level app provides a digital version of that experience by showing you exactly how much money you have to spend on a given day, week, or month. The main interface is just three bubbles that show you those numbers.

The Level app provides a digital version of that experience by showing you exactly how much money you have to spend on a given day, week, or month. The main interface is just three bubbles that show you those numbers.

The app’s features don’t stop there. You can also connect a number of (non-shitty) bank accounts to Level, and then the app keeps an up-to-the-minute log of your transactions. It also spots what’s a bill and factors in a monthly percentage of your income for a savings account. Level calls this feature Autosave.

Level is certainly not as complex as Mint, and that’s the beauty of it. If you’re living on a budget and want to figure out if that budget allows for a fancy dinner on a Friday night, you can do just that with one tap. Level also offers a feature called Insights that lets you track certain types of expenses and even expenditures at specific vendors. It looks like a fitness tracker for your wallet.

My dream bank…

…does not exist. I’ll be the first to admit that it’s a little bit silly to toggle between four different services in order to get a banking experience that doesn’t help buy more yachts for the 1 percent. But that’s the reality of it.

Many big shitty banks will offer checking and savings and financial planning and even mobile payments services. However, it all comes at a cost. These big shitty banks profit from the fees they charge you to use these products, and the time you spend on the phone trying to figure out what happened when things go wrong—and they will go wrong—is time you could be spending with your family. Or working—to make more money for your new, non-shitty bank account.

Illustration by Tara Jacoby